We have just returned from Washington, where we had the opportunity to meet with policymakers and investors during the IMF and World Bank Spring Meetings. Although this biannual gathering was once again marked by a high degree of uncertainty, policymakers from emerging economies appeared measured and pragmatic in their response, while investors showed a certain degree of optimism.

Public policy measures implemented since the onset of the conflict in Iran have broadly followed orthodox recommendations, with targeted and temporary fiscal policies aimed at mitigating inflationary risks and supporting demand. This improvement in policymaking across emerging and developing economies is all the more noteworthy given that such recommendations are now hardly implemented among developed countries. The broad-based strengthening of institutional frameworks across emerging markets over the past decade has notably given central banks the ability to remain patient while awaiting greater visibility.

While representatives from emerging economies are not showing signs of panic, they remain cautious and agree that the magnitude and duration of the supply shock linked to the conflict in Iran will be decisive for growth and inflation prospects. Both developed and emerging economies find it difficult to present clear baseline and alternative scenarios; however, a relatively swift resolution of the conflict appears to be the prevailing assumption. Should the conflict extend beyond the month of May, deteriorations in public finances combined with tighter-than-expected monetary restrictions would likely follow.

Investors broadly share this scenario of a rapid resolution to the conflict, with appetite for the asset class remaining strong — if not strengthening further. The unpredictability and threats of economic retaliation from the Trump administration toward longstanding US allies, once again evident in the context of the Iranian conflict, are contributing to investors’ growing desire for diversification.

This travel report focuses on four countries that, in our view, clearly illustrate the public policy improvements currently shaping our investment universe. We also present an initiative introduced by the London Coalition, whose mission is to deliver pragmatic solutions for sovereign finance and support countries in achieving their development ambitions. Such a proposal could further enhance the attractiveness of emerging sovereign debt relative to other public and private fixed-income asset classes.

Country Focus: ARGENTINA – Achievements and next steps of the economic program

Argentina’s government describes its economic program as one of the most ambitious and far-reaching reform agendas ever implemented within a democratic system. According to officials, the country is now experiencing its most promising economic outlook in decades after enduring more than 75 years of recurring crises, deep recessions, and chronic macroeconomic instability. This volatility significantly increased sovereign risk, discouraged long-term investment, and weakened economic growth. Reducing that instability became a central objective of the stabilization strategy.

The core of the program has been a major fiscal adjustment. Authorities argue that Argentina’s fiscal deficit represented the country’s main structural weakness. To address this issue, the government implemented a fiscal consolidation equivalent to roughly 5% of GDP in an exceptionally short period of time. Even the IMF initially considered such an adjustment impossible to achieve within a single year. Successfully carrying out these measures quickly strengthened the government’s credibility among international investors and financial institutions.

Another key pillar of the reforms has been the emphasis on the rule of law and the protection of contracts. The government opened the economy further while introducing a new framework intended to guarantee legal stability and property rights for foreign investors. Officials believe this institutional transformation has played a crucial role in restoring confidence and creating the conditions for what could become Argentina’s strongest economic expansion in decades.

Despite the severe interest-rate shock associated with stabilization policies, the banking system has remained resilient. Banks continue to be well-capitalized, and financial conditions are gradually improving. Short-term interest rates have fallen by approximately 15 percentage points since the beginning of the year, while long-term rates have also declined. Inflation expectations have dropped significantly, and expectations of currency depreciation remain relatively contained. Authorities interpret these developments as evidence that markets increasingly view the stabilization process as credible and sustainable.

At the same time, the central bank has managed to accumulate foreign exchange reserves despite the strengthening of the currency. Dollar deposits in the banking system have reached record levels of around USD 40 billion, reflecting the gradual return of capital previously held abroad by Argentine households and businesses. Officials argue that the economy has entered a virtuous cycle in which falling inflation, reserve accumulation, and macroeconomic stabilization reinforce one another.

The government also insists that the adjustment program was designed to protect the poorest citizens. Future structural reforms are expected to further support economic growth. Starting in July, the construction of approximately 9,000 kilometers of roads is projected to stimulate activity, alongside labor-market reforms aimed at improving productivity and competitiveness.

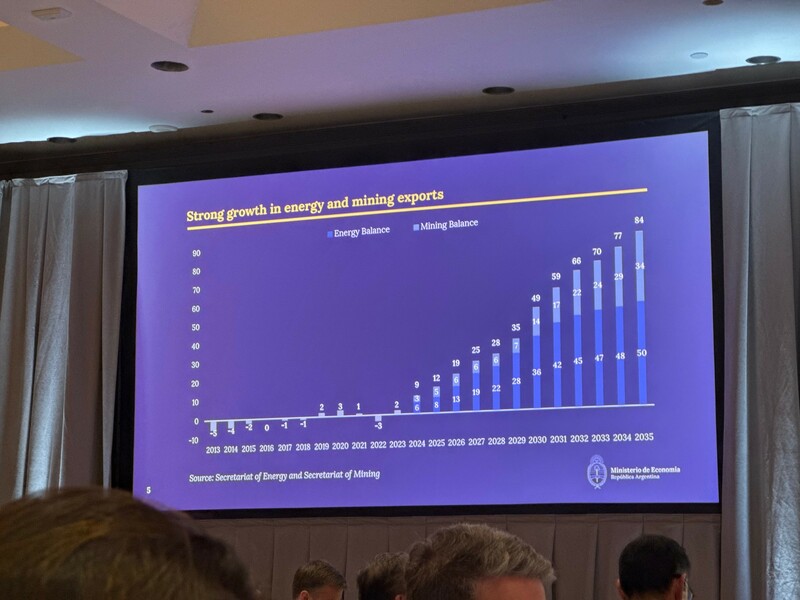

A major component of Argentina’s long-term strategy is the transformation of its export base. Historically dependent on agricultural exports, the country is increasingly focusing on energy and mining. Authorities estimate that these sectors could generate an additional USD 450 billion in exports over the next decade, with a large share of the necessary investments already approved or close to approval. Officials emphasize that these future export revenues would greatly exceed Argentina’s external debt obligations.

Regarding financing, the government stated that it is exploring alternatives to borrowing at current market rates and may partly rely on asset sales. Officials believe Argentina may not need to return to international capital markets for roughly eighteen months.

The government identifies the main risk as a possible return of populist economic policies. However, officials remain confident that such a reversal is unlikely, arguing that the country has moved from near economic collapse toward renewed growth and declining poverty. IMF forecasts predicting around 3.5% growth this year and even stronger growth next year further support the government’s optimistic outlook, despite continuing skepticism from some analysts and financial markets.

Country Focus: EGYPT – Increased resiliency to external shocks

Egypt’s economic strategy is currently centered on restoring fiscal sustainability while managing significant external and regional pressures. Policymakers are prioritizing a reduction in debt-servicing costs and an extension of debt maturities, rather than relying on further aggressive fiscal tightening. The government already runs a very large primary surplus—around 3.5% of GDP over the first nine months of the fiscal year—and considers a range of 4–5% of GDP to be an upper bound that should not be exceeded. Public debt remains elevated at roughly 81% of GDP, but authorities argue that this level should be assessed in comparison with peer countries that carry similar or even higher debt burdens. Despite these improvements, interest payments continue to absorb a large share of revenues, limiting the visible reduction in fiscal pressure for now.

External conditions remain a major source of vulnerability. The regional conflict in the Middle East has not yet severely disrupted fiscal performance, but it is exerting pressure on external balances. Portfolio outflows have reached roughly USD 14 billion from earlier peaks, reducing non-resident holdings significantly, particularly in Treasury bills. At the same time, the current account deficit is expected to widen—from around USD 19.5–14.5 billion in earlier estimates to roughly USD 21–22 billion—driven mainly by a deteriorating energy balance and weaker foreign exchange earnings from key sectors. Revenues from the Suez Canal have fallen sharply, by as much as 60% compared with 2023, while tourism could decline by up to 25% if the regional conflict persists. These negative factors are partially offset by record remittance inflows, which are running at an annualized level of around USD 42 billion.

Despite these pressures, policymakers emphasize that Egypt is better positioned than during previous global shocks, such as the 2022 energy crisis. A more flexible exchange rate regime, tighter monetary policy, and higher foreign exchange reserves have improved resilience. The Central Bank of Egypt has adopted an inflation-targeting approach rather than defending a fixed exchange rate, which authorities believe has strengthened credibility and helped stabilize portfolio inflows. Inflation, however, has risen to around 15.2% year-on-year, delaying a return to single-digit levels until potentially 2027, and the central bank remains ready to tighten policy further if inflation becomes entrenched.

On the financing side, Egypt continues to benefit from diversified external support. The International Monetary Fund has recently disbursed around USD 1.6 billion under its ongoing program, while Egypt retains access to Eurobond markets with potential issuance capacity of USD 1.5–2 billion at yields of approximately 7–7.5%. In addition, Gulf Cooperation Council commitments remain stable, providing a key financial backstop for the economy. Together, these flows help sustain liquidity in foreign currency markets despite episodes of capital outflows.

Beyond macroeconomic stabilization, the government is pushing an ambitious structural reform agenda to improve the investment climate. Efforts focus on reducing bureaucracy, digitalizing administrative processes, and simplifying business creation. Officials acknowledge that starting a business can still take up to six months, far longer than in competing economies, and see this as a major constraint on investment and job creation. Industrial expansion is also a priority, with plans to increase the number of investment parks beyond the current seven, although new developments will take time.

Privatization is another key pillar of reform, with upcoming initial public offerings of major state-owned assets aimed at deepening capital markets and attracting foreign investors. Authorities are also seeking to diversify foreign direct investment beyond traditional Gulf partners, with growing interest from European and Turkish investors. Overall, Egypt’s policy mix combines fiscal discipline, external financing support, and structural reforms, while navigating a challenging external environment marked by conflict-driven shocks, higher energy costs, and volatile capital flows.

Country Focus: PANAMA – Fiscal discipline with economic expansion

Panama’s government is pursuing an ambitious fiscal consolidation strategy aimed at achieving 4.4% GDP growth while cutting the fiscal deficit in half. Authorities insist that fiscal consolidation is already producing tangible results: government arrears have been reduced by half, improving liquidity conditions for SMEs and supporting employment. Despite a difficult external environment, the government expects to record its first primary surplus in 15 years this year.

Public revenues increased by 9%, while Panama Canal revenues rose by 26%, supported by a recovery in canal traffic from 36 to 42 ships per day since the recent drought-related disruptions. “Surgical” spending cuts target inefficiencies without undermining growth. Total public debt stands at roughly USD 60 billion, with debt servicing costs below 5% of GDP, among the lowest spreads in the region. Discussions with rating agencies remain constructive, with officials highlighting that Moody’s removed its negative outlook last year and recognized the government’s reform efforts.

The fiscal deficit target for 2026 is set at 3.5%, compared to an initial level of 3.75%. Authorities emphasized that budget execution is monitored on a daily basis, allowing rapid expenditure adjustments whenever revenue underperforms. The government benefits from significant operational flexibility, as many spending decisions can be adjusted without requiring approval from Congress or the cabinet.

Rather than pursuing a formal tax reform, the administration is focusing on improving tax compliance and reducing evasion. Officials stressed the political importance of ensuring everyone pays taxes before considering any increase in tax rates. The government is also reassessing long-standing subsidies and incentives for companies, arguing that businesses should not become permanently dependent on state support. Some subsidy programs have existed for over twenty years and are increasingly viewed as outdated.

A newly announced relief package is targeted primarily at low-income households and includes support for public transportation, school transportation, agriculture, and basic food products. Since Panama imports all of its oil, high energy prices remain a major vulnerability. However, officials believe that the increase in canal revenues could offset much of the cost of these targeted support measures.

Water security has become a major strategic priority. Authorities are more concerned about water shortages than physical threats to the Panama Canal itself. The government is therefore planning to build a second water reservoir to reduce drought risks and secure long-term canal operations. The project is expected to be financed by the Panama Canal Authority, which holds significant excess liquidity.

Mining policy remains politically sensitive. Arbitration over the suspended mine project is still ongoing, but officials noted that public opinion has shifted significantly, with support for reopening the mine now estimated at around 60%. The government argues that doing nothing is no longer a viable option and insists that any future agreement would generate at least double the revenues of the previous contract that was struck down by the Supreme Court. Authorities also stressed that reopening the mine would not necessarily require new legislation, as the Constitution already permits the state to exploit mineral resources.

Finally, Panama is expected to issue approximately USD 1.5 billion in external debt this year, while continuing efforts to deepen the domestic capital market and preserve macroeconomic stability within its fully dollarized economy.

Country Focus: MEXICO – Unlocking potential growth

Mexico’s economy has faced a series of external shocks in recent quarters, including higher oil prices, global trade tensions, and weaker external demand. Despite this challenging environment, authorities argue that the economy has remained relatively resilient. Exports have continued to perform reasonably well even after tariff-related disruptions, although officials acknowledged that headline export strength masks underlying domestic weakness. Much of Mexico’s export growth comes from sectors such as electronics and computers, where imported intermediate goods account for a significant share of production. As a result, export growth contributes positively to the trade balance but generates relatively limited domestic value added.

At the same time, uncertainty has weighed on both investment and household consumption. Businesses and consumers have increased savings and delayed spending decisions, reducing domestic demand momentum. Nevertheless, policymakers emphasized that private-sector balance sheets remain relatively healthy, creating the potential for a stronger rebound once uncertainty fades. Lower-income households are considered relatively protected thanks to accumulated savings and government social programs.

To support growth, the government plans additional infrastructure investment equivalent to roughly 2% of GDP. Authorities estimate that these projects could add around 1 percentage point to GDP growth, mainly in 2026 and 2027. Growth expectations for the current year have already been revised upward from 1.8% to 2.3%. Most infrastructure projects have already been approved, although officials noted that the approval and financing process for large-scale projects in Mexico remains lengthy and bureaucratic. The future of the USMCA also remains a major source of uncertainty for investors and policymakers.

Energy policy and the oil price shock were central topics of discussion. The government has attempted to offset higher energy prices through a combination of increased revenues from Pemex and adjustments to fuel excise taxes to cushion the impact on consumers. Officials argued that fuel demand in Mexico is relatively inelastic, making this mechanism effective as a temporary stabilizer. The policy is expected to be removed once oil prices normalize. Authorities also stressed that monetary policy should react appropriately to any second-round inflationary effects generated by higher energy prices.

A key government priority is the restructuring and recovery of Pemex. Authorities aim to reduce the company’s financing costs by refinancing expensive short- and medium-term debt and reducing reliance on costly bank credit lines. Improving Pemex’s credit profile is seen as essential to allowing the company to return to financial markets at lower borrowing costs. The government also intervened to support suppliers that had become dependent on expensive financing vehicles, although officials stressed that guarantees would only be provided for economically viable projects. Policymakers repeatedly emphasized that improving Pemex’s operational performance is critical not only for the energy sector but also for Mexico’s broader economic growth prospects.

Fiscal policy remains focused on gradual consolidation. The fiscal deficit is expected to decline from roughly 6% of GDP toward a range of 3–3.5%, although authorities admitted that the adjustment process has been delayed somewhat by recent shocks. Over the medium term, officials view a deficit closer to 4% of GDP as sustainable. Public debt may continue rising modestly in the near term, but authorities argued that Mexico does not face a debt sustainability problem. Instead, the priority is reducing the financial cost of debt servicing. Depending on growth performance and the speed of fiscal consolidation, debt-to-GDP could stabilize around 55–57%.

The government also highlighted several structural reform priorities. A broad digitalization agenda aims to reduce informality, combat illegal activities, and improve efficiency in tax collection and public administration. Mexico is also seeking to position itself as a destination for additional data center investment as geopolitical tensions encourage global companies to diversify supply chains. However, officials acknowledged that attracting these investments will require substantial improvements in electricity generation and energy infrastructure. Authorities are additionally exploring unconventional oil extraction methods, including fracking, although it remains unclear whether foreign participation would eventually be permitted.

On the monetary side, officials from the Bank of Mexico adopted a more cautious tone in response to recent inflationary pressures. One policymaker explicitly stated opposition to the latest 25bp interest-rate cut, arguing that recent commodity-price shocks justify greater prudence. Mexico imports approximately 75% of its fertilizer consumption, leaving the country highly exposed to global commodity prices. Products such as corn tortillas carry significant weight in the consumer basket and react rapidly to increases in agricultural commodity prices.

Although core inflation has behaved relatively well after excluding tax-related distortions, services inflation remained persistent throughout 2025 and became the main driver of inflation dynamics. Real ex-ante interest rates are estimated near 3%, close to neutral levels. Given ongoing uncertainty, several Banxico officials argued that a “wait-and-see” approach is appropriate. Some policymakers also suggested that previous forward guidance may have appeared overly dovish and that communication may need to become more hawkish going forward.

Banxico reiterated that its primary mandate remains inflation control, while acknowledging the government’s fiscal consolidation efforts and temporary measures to cushion energy-price shocks. Officials also explained that formal employment data provides a better measure of labor market conditions than the unemployment rate because workers often move from the formal sector to informal employment during downturns, keeping unemployment structurally low

Market Focus: A proposal for an emerging market debt “pause clause”

The London Coalition on Sustainable Sovereign Debt is advancing efforts to strengthen crisis-management tools for emerging market sovereigns through the introduction of standardized “pause clauses” in sovereign bond contracts. Backed by the UK government and major private investors representing roughly 20% of the investor base, the initiative aims to improve resilience to external shocks while preserving market access and investor confidence.

The proposed mechanism is designed as a liquidity-management tool rather than a solvency solution. Its objective is to provide temporary breathing space during severe crises, reducing the risk of disorderly defaults and improving the predictability of sovereign debt restructurings. Inspired by precedents in countries such as Grenada, Barbados, and Sri Lanka, the Coalition seeks to move away from ad hoc restructuring approaches toward a more systematic and scalable framework.

Under the proposal, sovereign issuers would be able to defer interest payments for one year, typically equivalent to two semi-annual coupon payments. The clause could only be activated once during the life of a bond and is intended as a preventive stabilization mechanism. The structure combines flexible activation triggers with safeguards designed to preserve market discipline and protect investors.

Two activation pathways are envisaged. The primary mechanism would require a sovereign to declare a national emergency or request IMF emergency financing. Activation would also require formal documentation, investor consultations, and confirmation that at least 60% of other external creditors are providing comparable relief. Investors would retain the right to reject activation through a majority vote.

A secondary pathway would apply automatically in cases of severe and independently verified shocks. If a World Bank rapid assessment estimates economic losses exceeding 15% of GDP, the clause could be triggered automatically without investor opt-out, while maintaining other contractual protections.

Beyond the pause clause itself, the Coalition is also working on broader reforms to improve transparency and coordination in sovereign debt restructurings, including private-sector non-bonded loans. The goal is to reduce delays, improve predictability, and strengthen confidence across creditor groups during crises.

Supporters argue that any potential cost associated with the clause should be offset by lower default risks, stronger transparency standards, and improved long-term credit quality. The mechanism is also designed to minimize unintended market disruptions, notably by avoiding credit default swap triggers in most cases, since payments are deferred rather than missed.

Overall, the proposal seeks to create a more resilient sovereign debt architecture for emerging and frontier economies exposed to climate, geopolitical, and macroeconomic shocks, while preserving market discipline and limiting additional financing costs.

Guillaume Riteau

Fund Manager - Gemway Assets