The current conflict in Iran has two negative consequences for emerging markets in the short term :

- Rise in US dollar, typically seen as a safe haven currency in this type of situation ;

- Rise in oil and gas prices due to the de facto closure of the Strait of Hormuz (20% of crude i.e 20mn b/d) of which about 1/4th can find alternative routes.

It should be noted, of course, that securing this passage is a priority for the US and Israeli forces. President Trump appears to be committed to this. He has also announced the US International

Development Finance Corp will assure tankers as they cross the strait.

It should be noted that current global stocks are high (around 6.5 billion barrels, including 3.5 billion barrels outside the Persian Gulf). Given the shortfall caused by the closure of the strait (around 70% of 20mn barrels per day), the global economy can hold on for around 200 days (an approximate calculation).

Among the most affected countries, we must not forget Iran itself, which derives 80% of its tax revenue from sale of crude. These sales are mainly to China and account to 10% of Chinese crude imports.In terms of price impact (oil +15% in the past 3 days) and the impact on global activity, all emerging market countries are affected.

Specifically in terms of supply, the most affected countries are in Asia:

- Oil: Korea, Taiwan, Thailand, Philippines and China

- Gas: India

In the past 3 days, the Asian markets have witnessed a steep fall: -18% in Korea, -11% in Thailand, -8% in Indonesia and Philippines, -7% in Taiwan, -6% in Hong Kong, -3% in Chi na (A shares) and -3% in India. Many stocks have fallen between 15 and 25%, particularly stocks which had risen sharply during the first two months of 2026. This was the case with Samsung Electronics, SK Hynix and Hyundai Motors. The same applies to Taiwanese companies such as ASE Technology (-15%), Delta (-12%) and Hon Hai (-11%). TSMC is playing its role as a defensive stock, falling "only by" 7%. Elsewhere, in Latin America and the Middle East the declines have been smaller (-3% in Brazil, -4% in Mexico, -1% in Saudi Arabia, -4% in the UAE). These falls were also accompanied by currency losses against the dollar. However, as the euro also fell against the dollar, the impact expressed in euros was mixed.

na (A shares) and -3% in India. Many stocks have fallen between 15 and 25%, particularly stocks which had risen sharply during the first two months of 2026. This was the case with Samsung Electronics, SK Hynix and Hyundai Motors. The same applies to Taiwanese companies such as ASE Technology (-15%), Delta (-12%) and Hon Hai (-11%). TSMC is playing its role as a defensive stock, falling "only by" 7%. Elsewhere, in Latin America and the Middle East the declines have been smaller (-3% in Brazil, -4% in Mexico, -1% in Saudi Arabia, -4% in the UAE). These falls were also accompanied by currency losses against the dollar. However, as the euro also fell against the dollar, the impact expressed in euros was mixed.

India and China are the least affected countries in Asia. After 15 months of under-performance, the former in general is underweighted by most international investors, who are selling less in this market. From an economic perspective, India, particularly its petrochemical industry would severely be impacted by the lack of liquefied natural gas (mainly sourced from Qatar). As for the latter, she has significant strategic oil reserves, which enable her to mitigate the short-term quantitative impact. China can also implement rapid fiscal stimulus measures to support local activity. In this regard, announcements are expected in the coming days following the NPC’s 2 sessions in early March. Beijing could announce measures to boost local activity, consumption and investment.

In this geopolitical environment, it is difficult to establish a clear scenario. The US and Israel are evidently in favor of short intervention, lasting for around 4-5 weeks. At the same time, the death of a significant number of Iranian leaders during the operation means it is impossible to have a clear picture of the country’s strategy, while the military chain of comma nd has been disturbed, if not dislocated. The most likely scenario at this point, which is also one of the most favorable, is a short military operation that destroys Iranian regime’s military capabilities and thereby restores security in the Strait of Hormuz. Conversely, the main risk is a prolonged conflict (with the Strait remaining insecure and Iran retaliating against facilities in neighboring countries). This scenario would quickly prompt us to review our investment strategy in favor of more defensive investments (domestic stocks in India, China, Latin America and Saudi Arabia).

nd has been disturbed, if not dislocated. The most likely scenario at this point, which is also one of the most favorable, is a short military operation that destroys Iranian regime’s military capabilities and thereby restores security in the Strait of Hormuz. Conversely, the main risk is a prolonged conflict (with the Strait remaining insecure and Iran retaliating against facilities in neighboring countries). This scenario would quickly prompt us to review our investment strategy in favor of more defensive investments (domestic stocks in India, China, Latin America and Saudi Arabia).

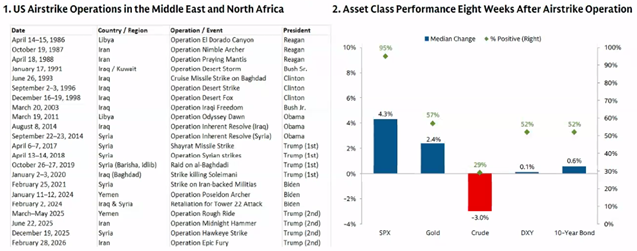

At the current juncture, it is important to remain cautious and avoid any negative overreaction to current events. It should be remembered that over the past four decades, there have been 21 conflicts in the Middle East. Each time, the scenario seems to be the same: short-term decline in markets, rise in oil prices and the dollar. Eight weeks later, stocks indices are higher in 95% of the cases. As far as we are concerned, we have not made any major changes to our allocation at this stage. However, the portfolio remains highly adaptable: 90% of the portfolio can be liquidated within 24 hours if necessary (100% for GemAsia and GemChina). This flexibility allows us to quickly increase the proportion of cash or rotate sectors depending on how the conflict develops. The price collapse makes semiconductors extremely cheap (2026 PER: Samsung Electronic 6.4x, SK Hynix 4.4x). TSMC is now at 15x, a level rarely reached by the Taiwanese leader.

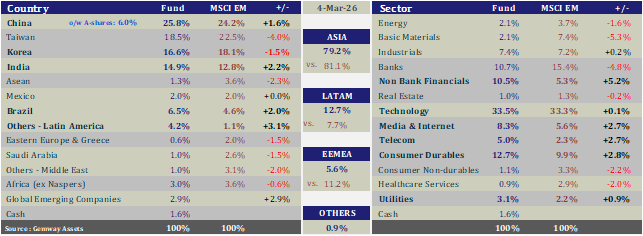

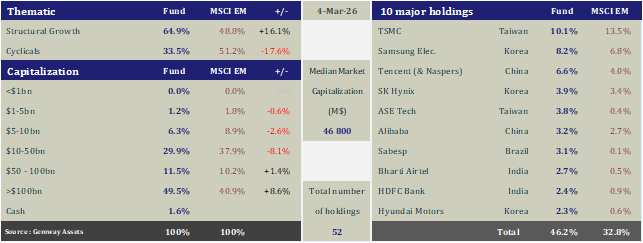

See below GemEquity’s geographical and sector breakdown as of March 4th 2026 :

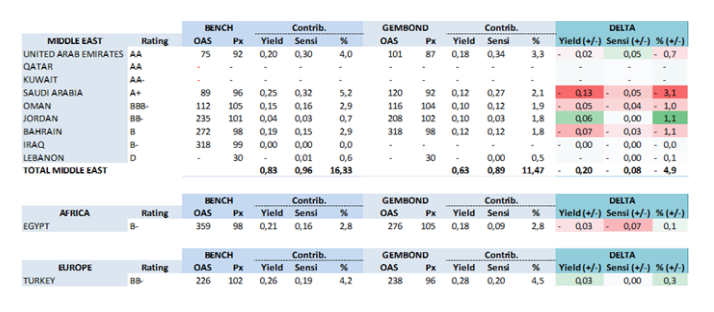

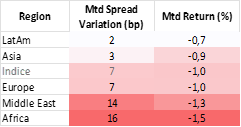

In emerging hard-currency bond markets, the reaction has been relatively contained, with the average risk premium widening by 7bp since Friday. Africa has been th e most affected region (+16bp), followed, unsurprisingly, by the Middle East (+14bp). Latin America and Asia have remained broadly unchanged (+2bp and +3bp respectively), while Europe has widened in line with the index. The 1% market decline is primarily attributable to the rates component (-0.6%) and concerns over a renewed inflationary shock, rather than to the credit component (-0.4%). The appreciation of the US dollar, typical during periods of risk aversion, has particularly impacted the localcurrency emerging debt market, which corrected by 2.9%.

e most affected region (+16bp), followed, unsurprisingly, by the Middle East (+14bp). Latin America and Asia have remained broadly unchanged (+2bp and +3bp respectively), while Europe has widened in line with the index. The 1% market decline is primarily attributable to the rates component (-0.6%) and concerns over a renewed inflationary shock, rather than to the credit component (-0.4%). The appreciation of the US dollar, typical during periods of risk aversion, has particularly impacted the localcurrency emerging debt market, which corrected by 2.9%.

Within the Middle East, the widening of sovereign risk premiums has followed the hierarchy of credit ratings, with a marked underperformance from Lebanon (+106bp) and Iraq (+68bp), followed to a lesser extent by Bahrain (+22bp) and Jordan (+15bp). The Sultanate of Oman, owing to its lower exposure to hydrocarbons and its historically neutral political stance in the region, has been the least affected (+6bp). Saudi Arabia and the United Arab Emirates have widened by 10bp. Qatar and Kuwait, which exited the index after being reclassified as developed countries, have widened by 8bp and 20bp, respectively. Performance figures, reflecting each country’s average duration, show greater resilience in Lebanon (-0.3%) and Iraq (-0.8%).

Regarding our bond fund, we have made no major changes to our allocation at this stage. Since the beginning of the year, we have been reducing our exposure to the Middle East (as well as to Egypt) by 2% to 11.5% (vs 16.3 in the index). It represents our second-largest regional underweight after Asia. For the time being, we are maintaining a significant liquidity buffer (8%) while awaiting greater visibility on the duration and outcome of the conflict.